Capítulo 6 VARIABLES EN EL TIEMPO, AJUSTE A MODELO LINEAL Y ESTACIONARIO

6.1 Modelo lineal

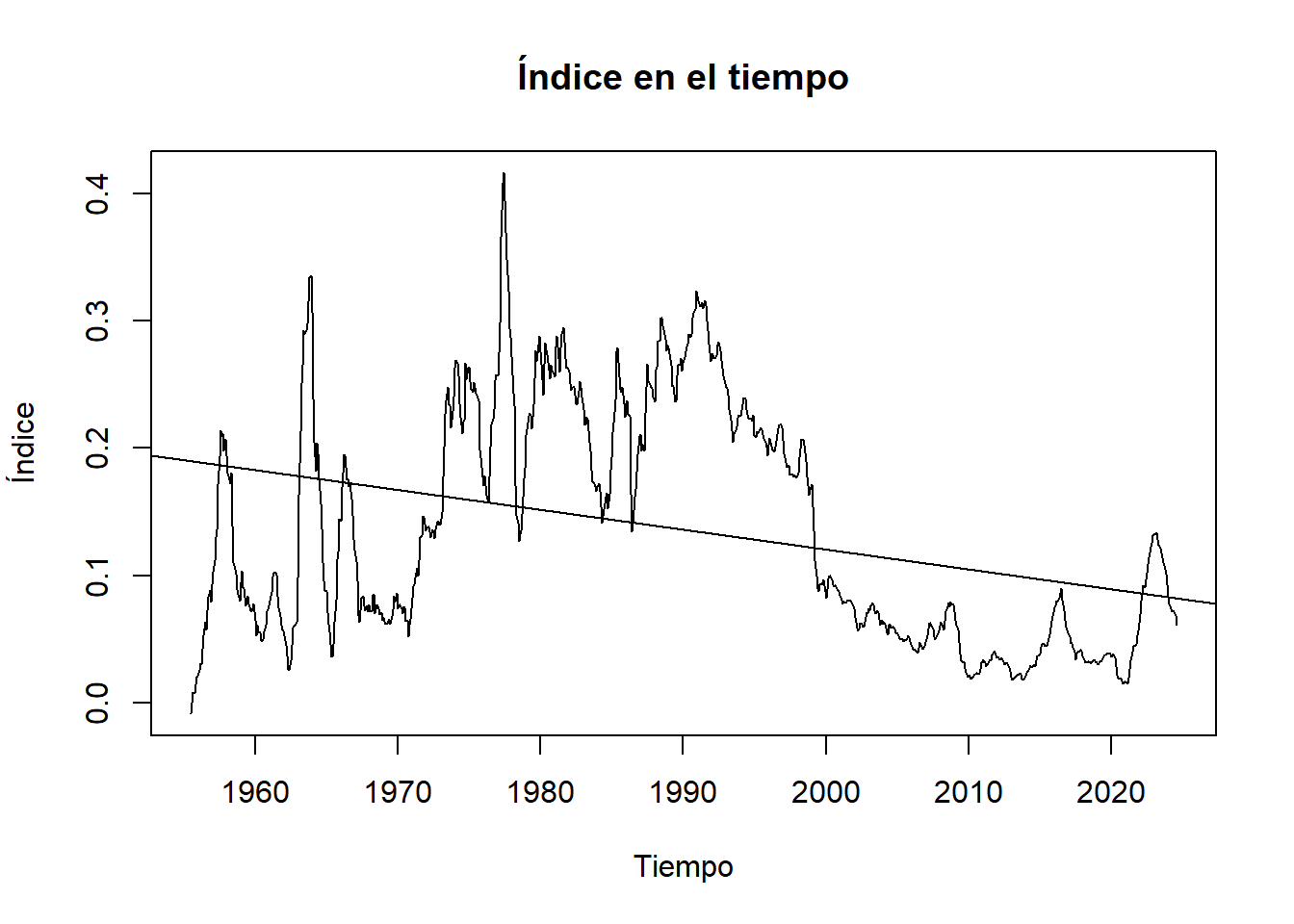

plot(Indice_ts, main="Índice en el tiempo", xlab="Tiempo", ylab="Índice")

abline(reg = lm(Indice_ts ~ time(Indice_ts)))

## Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

## 1955 7 8 9 10 11 12

## 1956 1 2 3 4 5 6 7 8 9 10 11 12

## 1957 1 2 3 4 5 6 7 8 9 10 11 12

## 1958 1 2 3 4 5 6 7 8 9 10 11 12

## 1959 1 2 3 4 5 6 7 8 9 10 11 12

## 1960 1 2 3 4 5 6 7 8 9 10 11 12

## 1961 1 2 3 4 5 6 7 8 9 10 11 12

## 1962 1 2 3 4 5 6 7 8 9 10 11 12

## 1963 1 2 3 4 5 6 7 8 9 10 11 12

## 1964 1 2 3 4 5 6 7 8 9 10 11 12

## 1965 1 2 3 4 5 6 7 8 9 10 11 12

## 1966 1 2 3 4 5 6 7 8 9 10 11 12

## 1967 1 2 3 4 5 6 7 8 9 10 11 12

## 1968 1 2 3 4 5 6 7 8 9 10 11 12

## 1969 1 2 3 4 5 6 7 8 9 10 11 12

## 1970 1 2 3 4 5 6 7 8 9 10 11 12

## 1971 1 2 3 4 5 6 7 8 9 10 11 12

## 1972 1 2 3 4 5 6 7 8 9 10 11 12

## 1973 1 2 3 4 5 6 7 8 9 10 11 12

## 1974 1 2 3 4 5 6 7 8 9 10 11 12

## 1975 1 2 3 4 5 6 7 8 9 10 11 12

## 1976 1 2 3 4 5 6 7 8 9 10 11 12

## 1977 1 2 3 4 5 6 7 8 9 10 11 12

## 1978 1 2 3 4 5 6 7 8 9 10 11 12

## 1979 1 2 3 4 5 6 7 8 9 10 11 12

## 1980 1 2 3 4 5 6 7 8 9 10 11 12

## 1981 1 2 3 4 5 6 7 8 9 10 11 12

## 1982 1 2 3 4 5 6 7 8 9 10 11 12

## 1983 1 2 3 4 5 6 7 8 9 10 11 12

## 1984 1 2 3 4 5 6 7 8 9 10 11 12

## 1985 1 2 3 4 5 6 7 8 9 10 11 12

## 1986 1 2 3 4 5 6 7 8 9 10 11 12

## 1987 1 2 3 4 5 6 7 8 9 10 11 12

## 1988 1 2 3 4 5 6 7 8 9 10 11 12

## 1989 1 2 3 4 5 6 7 8 9 10 11 12

## 1990 1 2 3 4 5 6 7 8 9 10 11 12

## 1991 1 2 3 4 5 6 7 8 9 10 11 12

## 1992 1 2 3 4 5 6 7 8 9 10 11 12

## 1993 1 2 3 4 5 6 7 8 9 10 11 12

## 1994 1 2 3 4 5 6 7 8 9 10 11 12

## 1995 1 2 3 4 5 6 7 8 9 10 11 12

## 1996 1 2 3 4 5 6 7 8 9 10 11 12

## 1997 1 2 3 4 5 6 7 8 9 10 11 12

## 1998 1 2 3 4 5 6 7 8 9 10 11 12

## 1999 1 2 3 4 5 6 7 8 9 10 11 12

## 2000 1 2 3 4 5 6 7 8 9 10 11 12

## 2001 1 2 3 4 5 6 7 8 9 10 11 12

## 2002 1 2 3 4 5 6 7 8 9 10 11 12

## 2003 1 2 3 4 5 6 7 8 9 10 11 12

## 2004 1 2 3 4 5 6 7 8 9 10 11 12

## 2005 1 2 3 4 5 6 7 8 9 10 11 12

## 2006 1 2 3 4 5 6 7 8 9 10 11 12

## 2007 1 2 3 4 5 6 7 8 9 10 11 12

## 2008 1 2 3 4 5 6 7 8 9 10 11 12

## 2009 1 2 3 4 5 6 7 8 9 10 11 12

## 2010 1 2 3 4 5 6 7 8 9 10 11 12

## 2011 1 2 3 4 5 6 7 8 9 10 11 12

## 2012 1 2 3 4 5 6 7 8 9 10 11 12

## 2013 1 2 3 4 5 6 7 8 9 10 11 12

## 2014 1 2 3 4 5 6 7 8 9 10 11 12

## 2015 1 2 3 4 5 6 7 8 9 10 11 12

## 2016 1 2 3 4 5 6 7 8 9 10 11 12

## 2017 1 2 3 4 5 6 7 8 9 10 11 12

## 2018 1 2 3 4 5 6 7 8 9 10 11 12

## 2019 1 2 3 4 5 6 7 8 9 10 11 12

## 2020 1 2 3 4 5 6 7 8 9 10 11 12

## 2021 1 2 3 4 5 6 7 8 9 10 11 12

## 2022 1 2 3 4 5 6 7 8 9 10 11 12

## 2023 1 2 3 4 5 6 7 8 9 10 11 12

## 2024 1 2 3 4 5 6 7 8

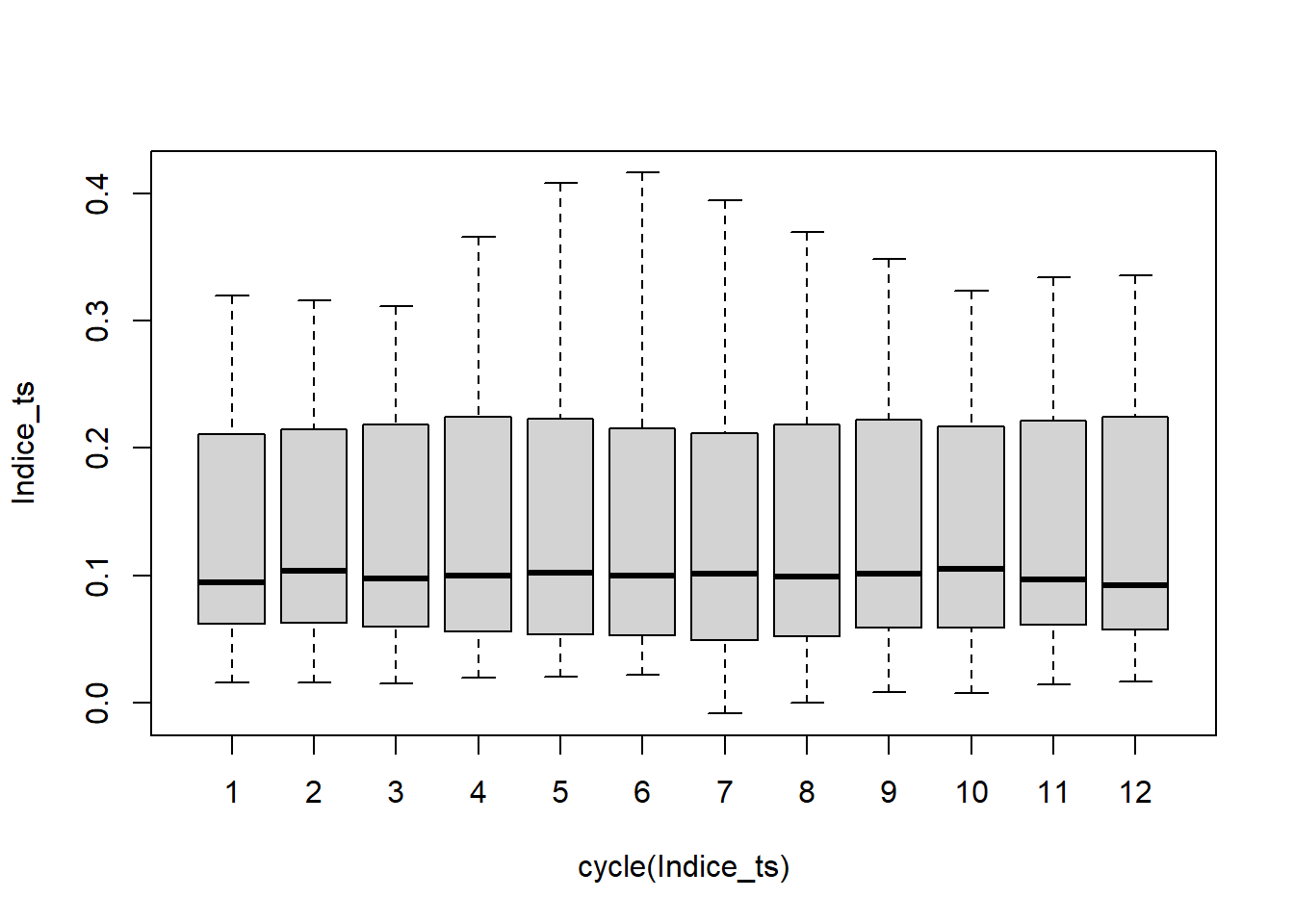

Se observan valores homegéneos en los meses y no se observan valores atípicos marcados.

Se observan valores homegéneos en los meses y no se observan valores atípicos marcados.

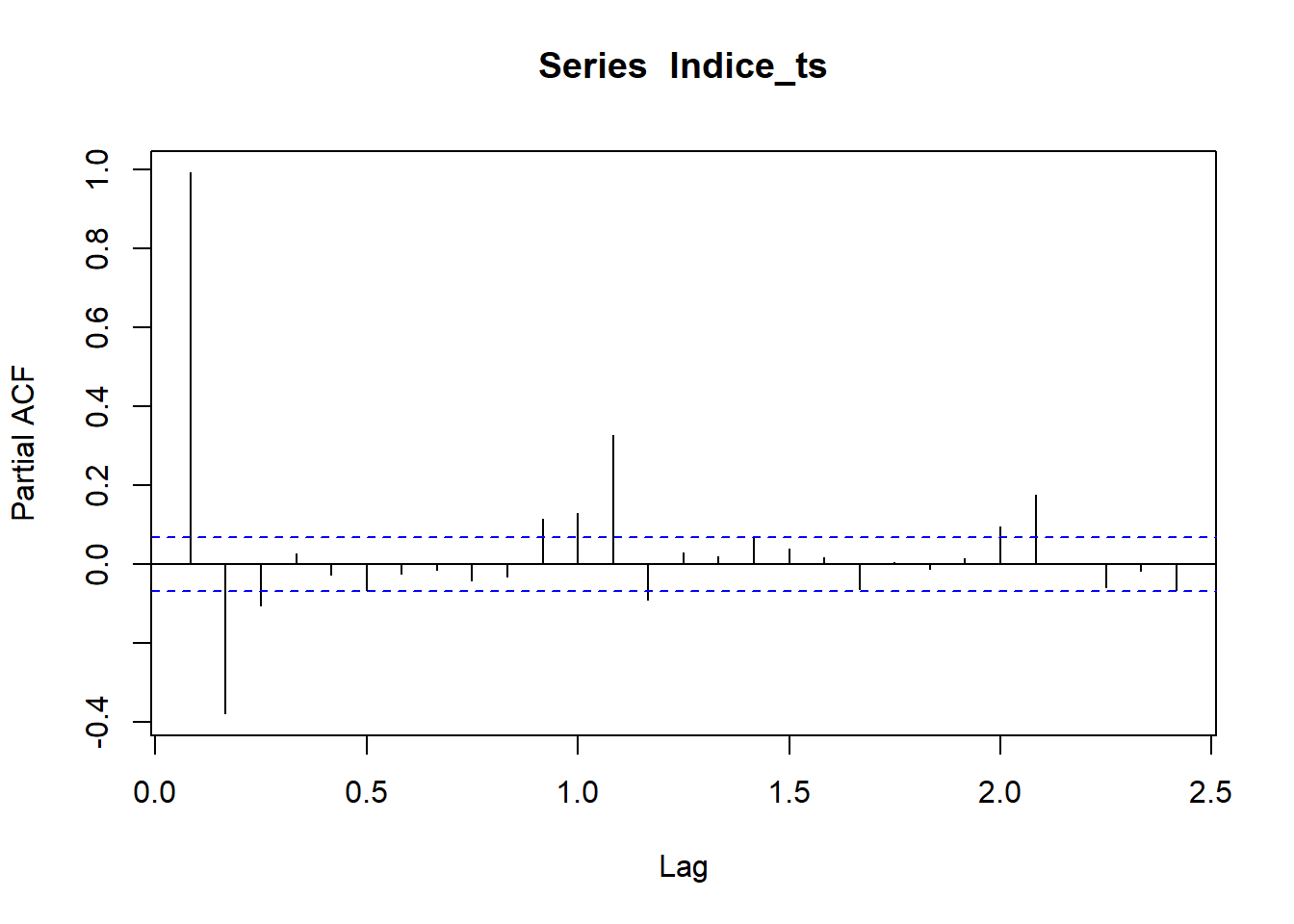

6.2 Modelo ARIMA

##

## OCSB test

##

## data: Indice_ts

##

## Test statistic: -51.3138, 5% critical value: -1.803

## alternative hypothesis: stationary

##

## Lag order 0 was selected using fixed

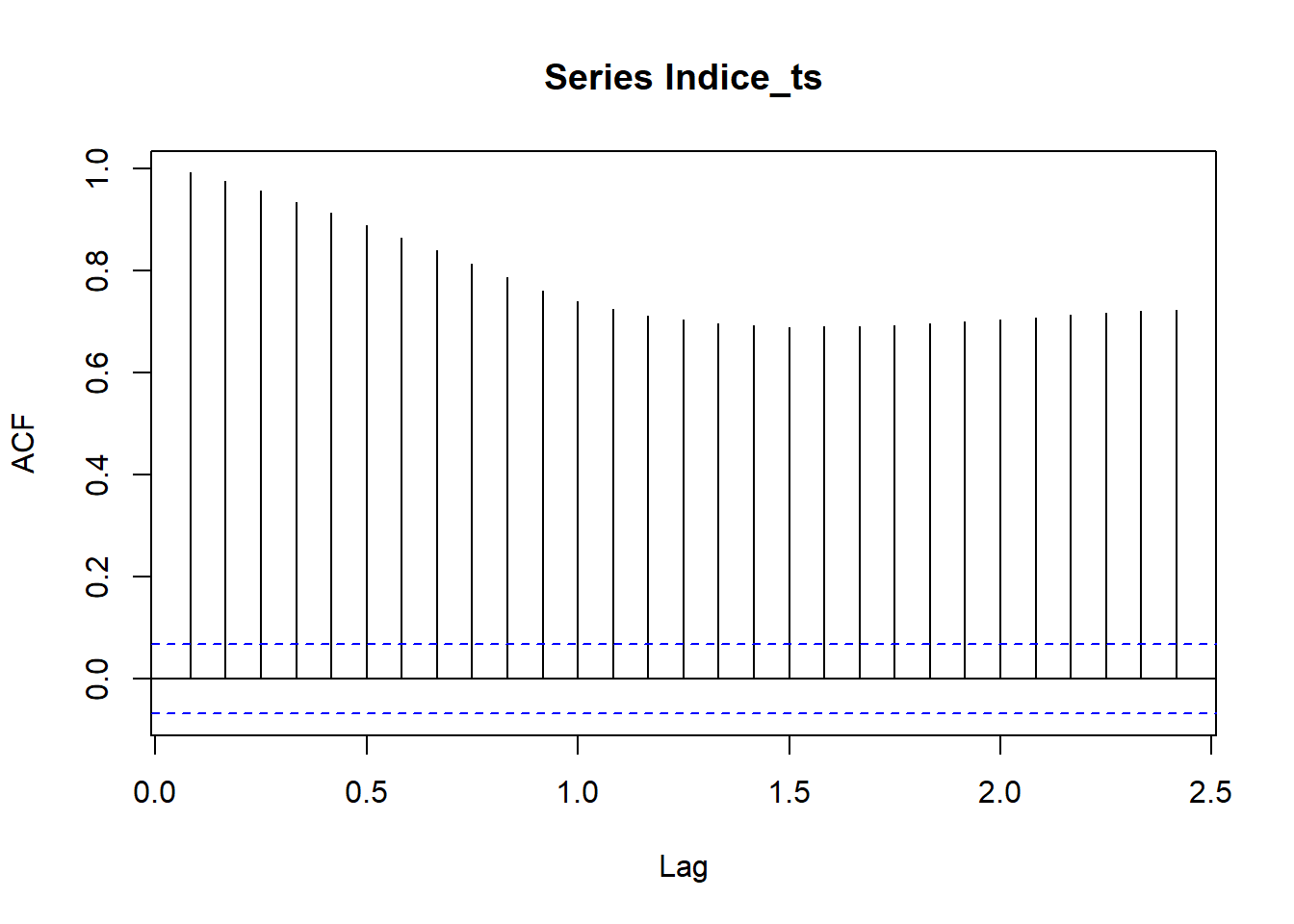

El componente estacional de Indice_ts no es significativo, debido a esto se aplicará el modelo ARIMA directamente.

Indice_ts_diff <- diff(Indice_ts)

resultado_adf_diff <- adf.test(Indice_ts_diff, alternative = "stationary") ## Series: Indice_ts_diff

## ARIMA(2,0,1)(0,0,2)[12] with zero mean

##

## Coefficients:

## ar1 ar2 ma1 sma1 sma2

## 0.1628 0.3147 0.3815 -0.8884 0.0833

## s.e. 0.2118 0.1230 0.2159 0.0373 0.0375

##

## sigma^2 = 5.259e-05: log likelihood = 2903.25

## AIC=-5794.5 AICc=-5794.4 BIC=-5766.18

##

## Training set error measures:

## ME RMSE MAE MPE MAPE MASE ACF1

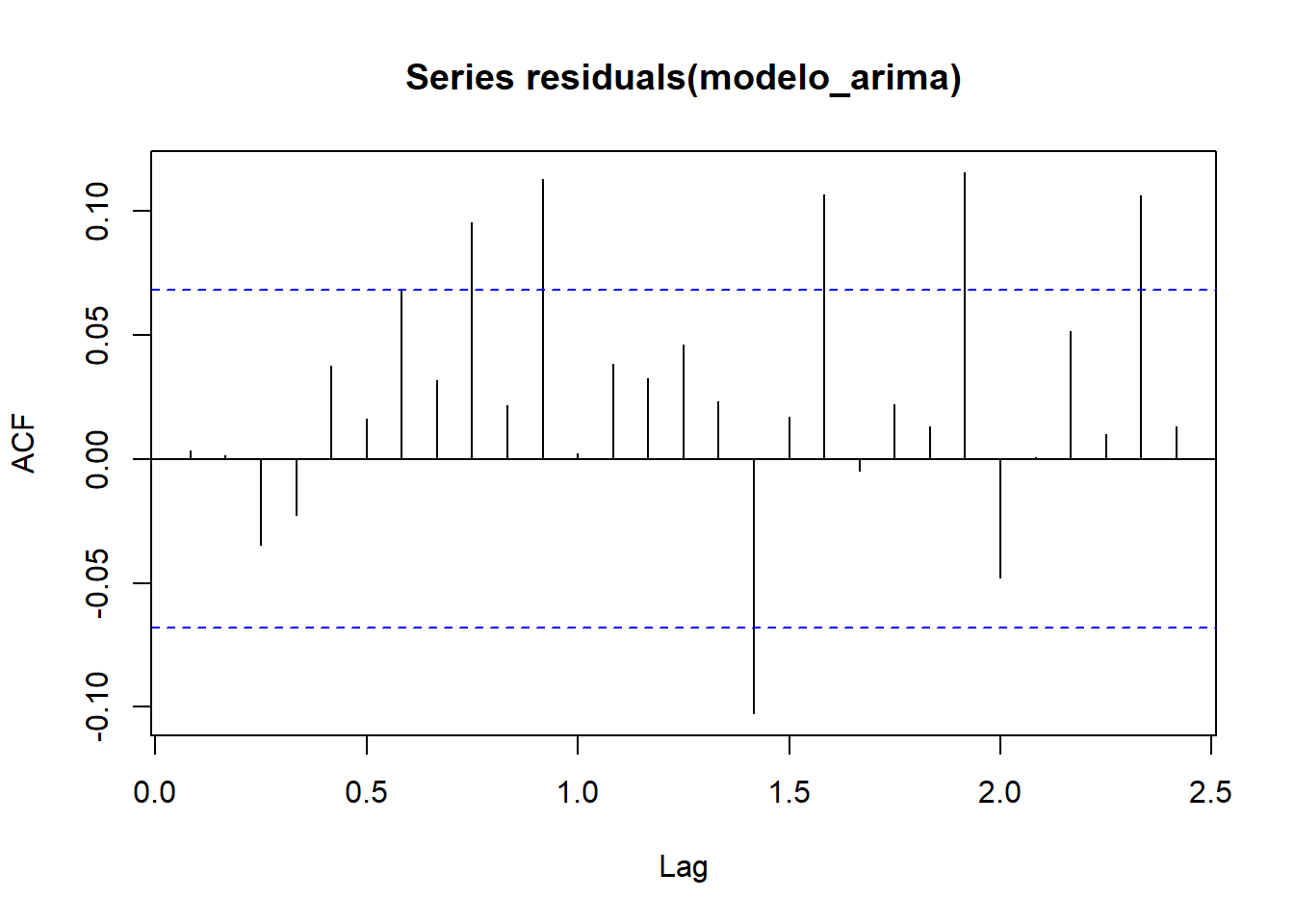

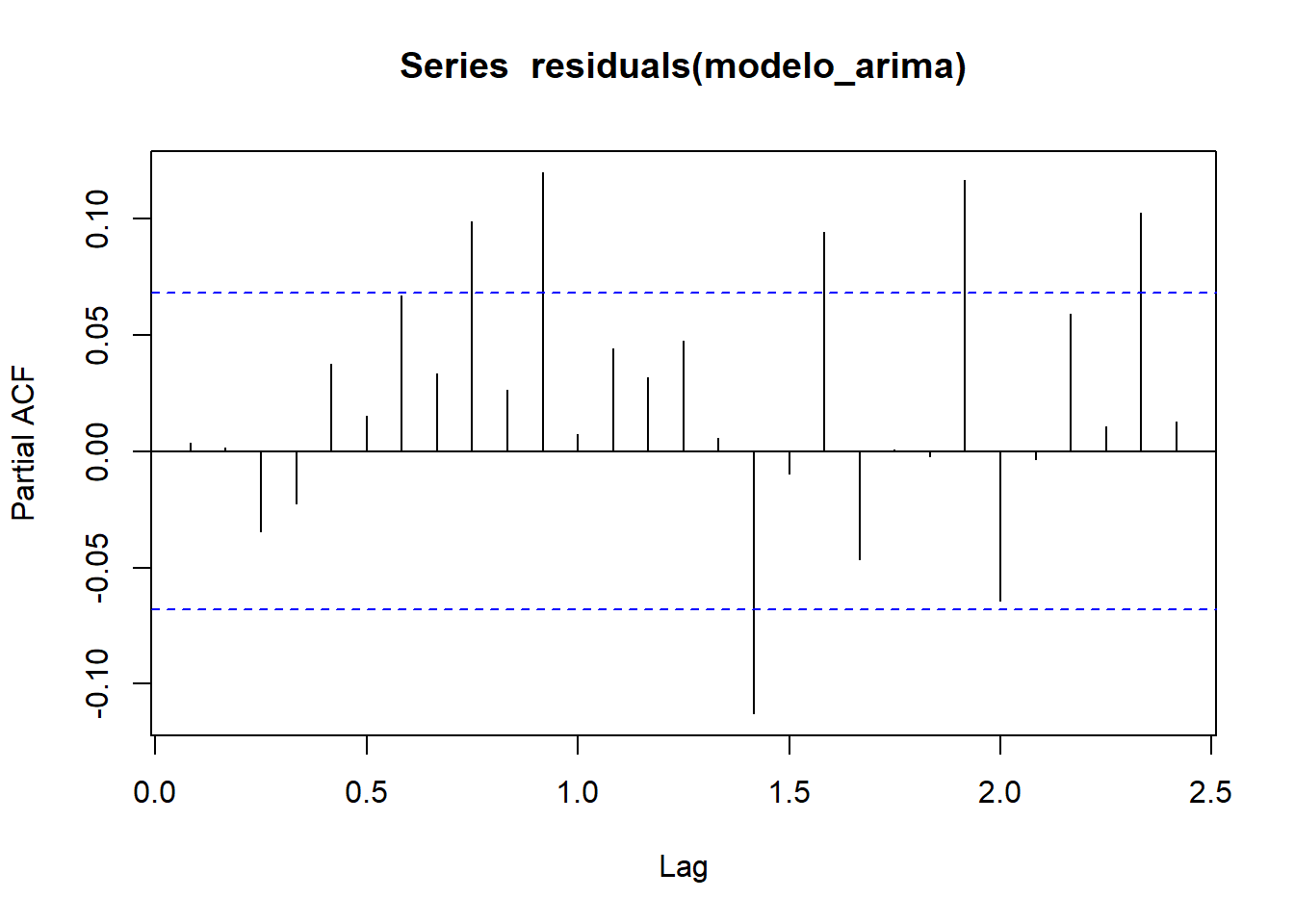

## Training set 4.972306e-05 0.0072301 0.004844645 NaN Inf 0.3930951 0.0034672456.2.1 Test de residuos, AFC y PACF

##

## Box-Ljung test

##

## data: residuals(modelo_arima)

## X-squared = 0.010002, df = 1, p-value = 0.9203

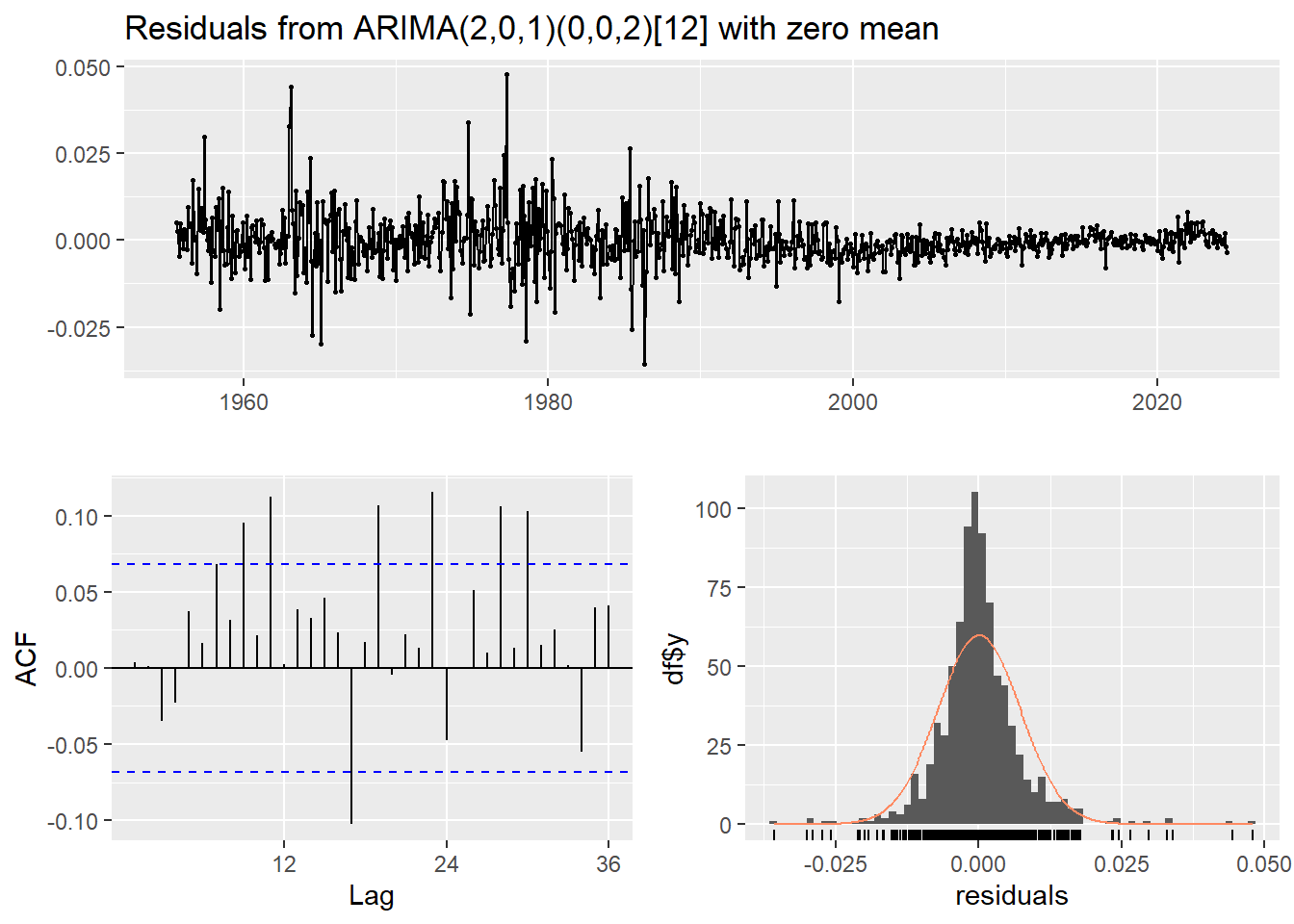

De acuerdo con los resultados obtenidos, el p-value es mayor que 0.05, por lo que los residuales se pueden considerar como ruido blanco y el modelo representa bien la estructura de la serie de tiempo.

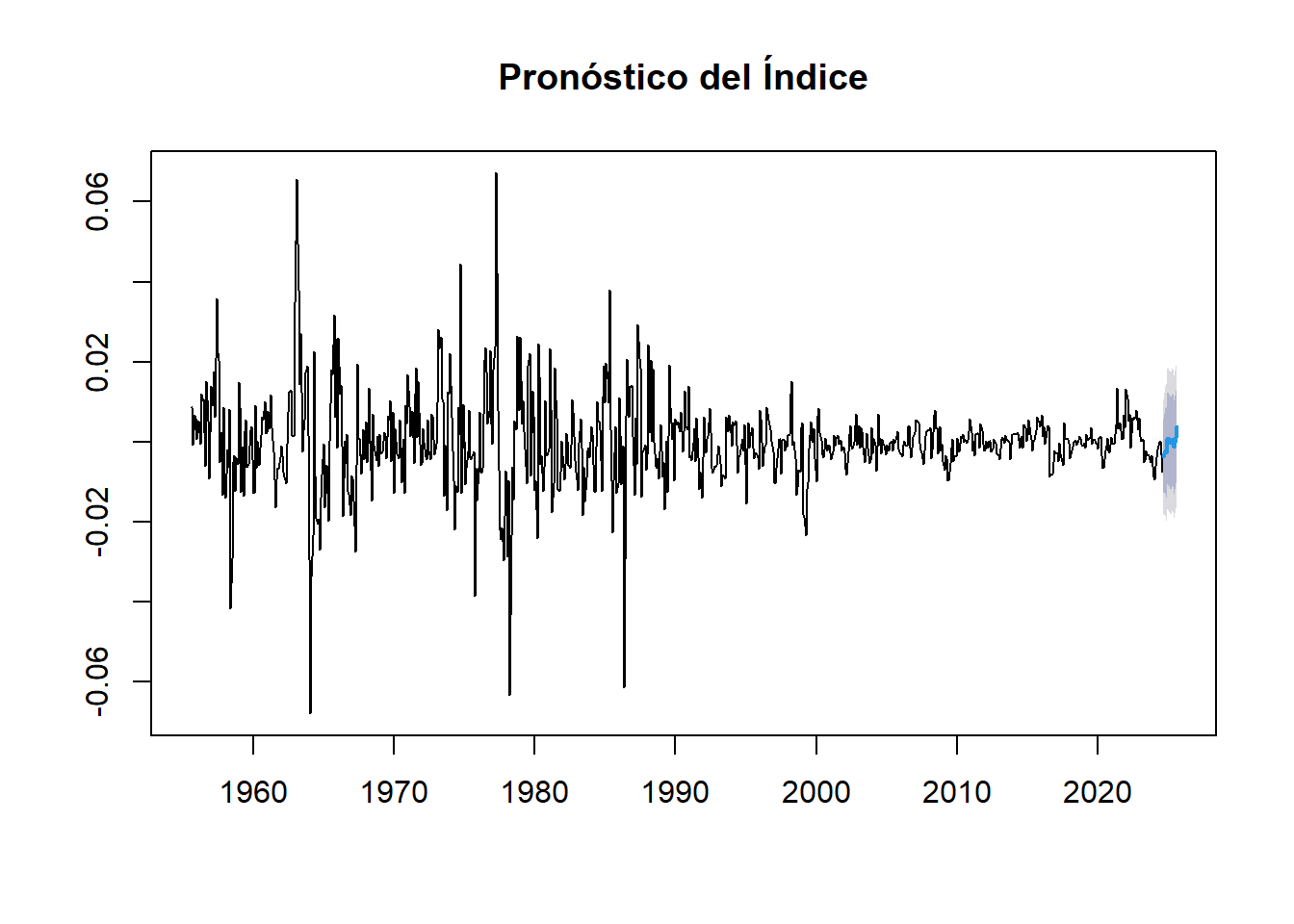

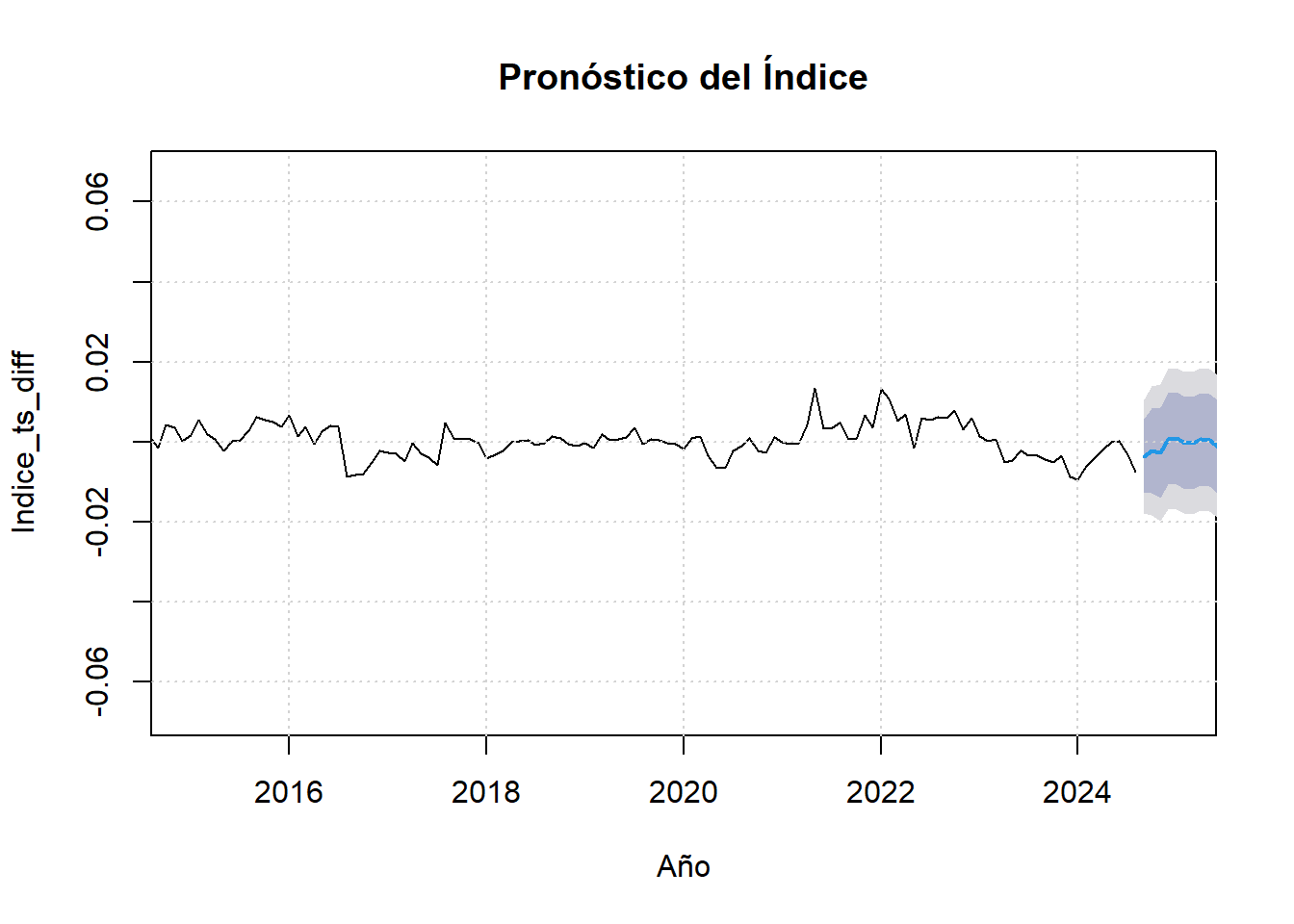

6.2.2 Pronóstico

forecast_data <- forecast::forecast(modelo_arima, h = 12)

plot(forecast_data, main = "Pronóstico del Índice")

plot(forecast_data, main = "Pronóstico del Índice", xlab = "Año", ylab = "Indice_ts_diff", xlim = c(2015, 2025))

grid()

6.2.3 Resultados

##

## Ljung-Box test

##

## data: Residuals from ARIMA(2,0,1)(0,0,2)[12] with zero mean

## Q* = 63.564, df = 19, p-value = 1.043e-06

##

## Model df: 5. Total lags used: 24##

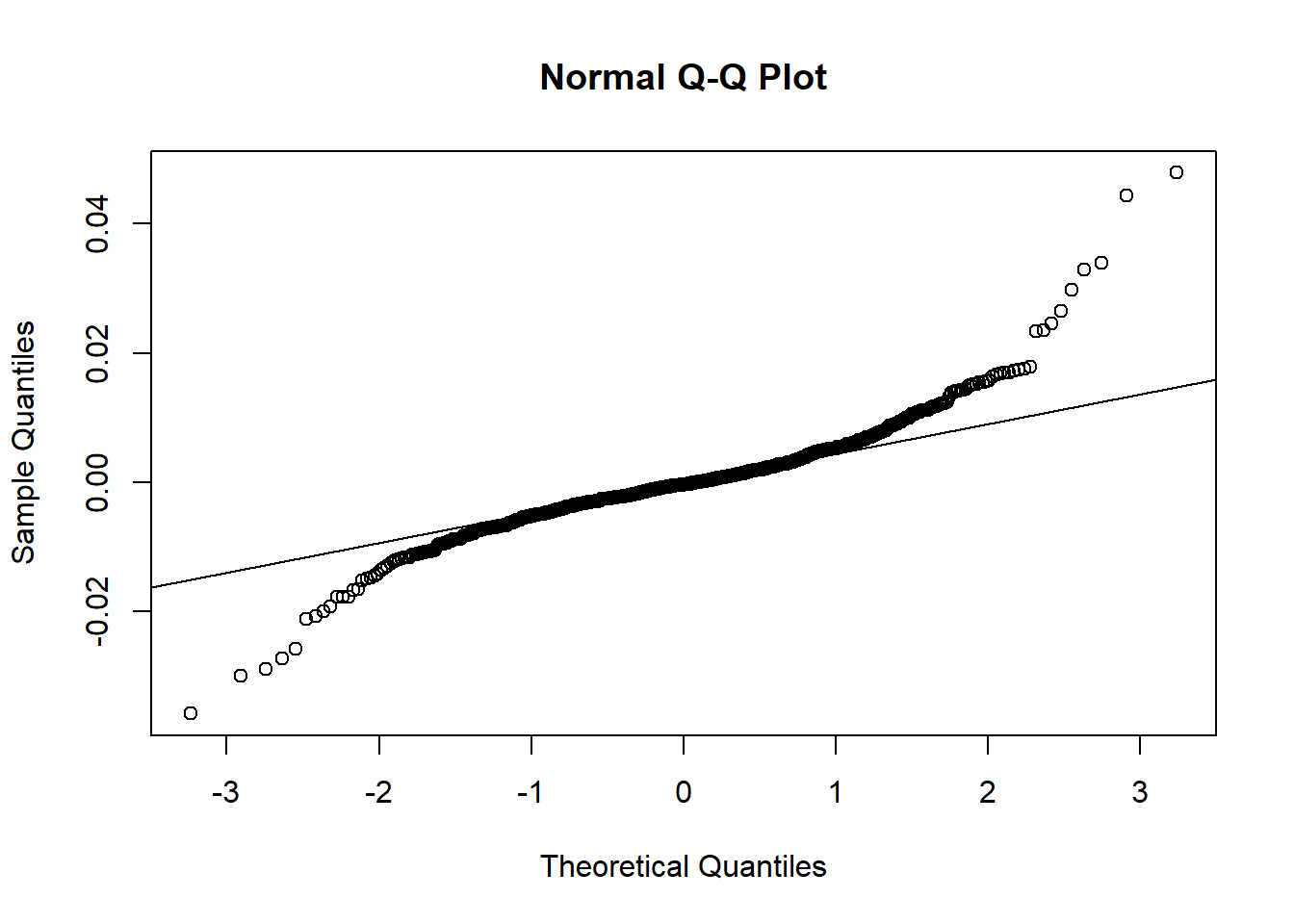

## Shapiro-Wilk normality test

##

## data: residuales

## W = 0.91174, p-value < 2.2e-16El valor de 0.91174 sugiere que los residuales están algo alejados de seguir una distribución normal, lo cual se confirma con el p-value bajo.

##

## Box-Ljung test

##

## data: residuales

## X-squared = 0.010002, df = 1, p-value = 0.9203El valor X-squared bajo, indica que hay poca correlación en los residuales y dado que el p-value es alto, significa que los residuales pueden ser considerados como ruido blanco.